Calibration with Implied Volatility

for Equity Indexes

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

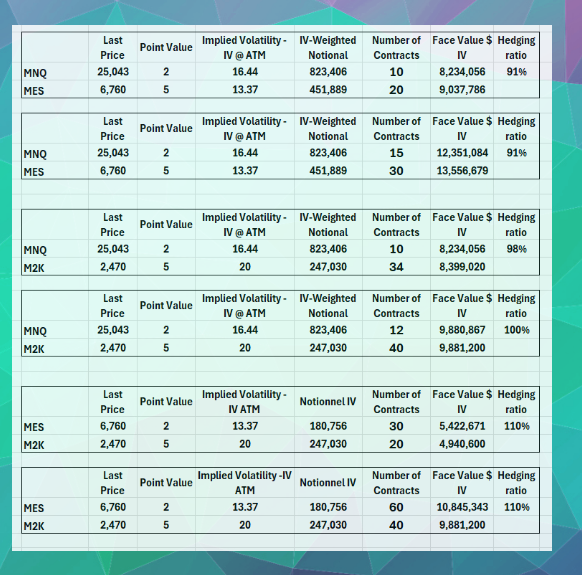

🎯 Calibrating 2-Leg Strategies on S&P 500 & Nasdaq

With Implied Volatility Correction (Based on 0-DTE ATM Options)*

💈 How to use this sheet

Updated on 5th Oct 25. This Implied Volatility Calibration is correct until next update

💈 The Essentials of Spread Trading: What Every Trader Should Know

When calibrating index spreads like the S&P 500 (ES) against the Nasdaq (NQ), it's not enough to just balance the point values.

We go further — by adjusting for Implied Volatility (IV) to reflect current market sentiment and price behavior.

Here’s how it works:We monitor the At-The-Money (ATM) IV of 0-DTE options — even though we’re trading the futures contracts, not the options directly.

Why? Because 0-DTE option flows influence intraday futures behavior, and IV gives us insight into how aggressively each index might move.

This approach allows you to scale into spreads with greater precision, entering more or less aggressively on the hedge leg depending on the IV imbalance between ES and NQ.Yes — it can sound complex at first.

But you don’t have to figure it all out alone:

👉 Train with JP Ferra or ask your question directly — we’ve mapped out a range of scenarios to help you mix Micro and Mini contracts with confidence.

💈 How to use this sheet

When establishing a trade, options traders have the flexibility to choose the Delta of their Calls and Puts—ranging from +100 to -100—to match their desired exposure and directional bias.In contrast, futures traders are limited to a Delta of +50 or -50 per contract, offering less flexibility in fine-tuning directional exposure. Because of this, it’s even more important to actively manage risk.At Structure-Trading.com, we believe it's wise to offset 50% of your risk when your "heavy side" begins to generate profit. This approach helps lock in gains while reducing downside exposure—keeping your capital protected and your strategy disciplined.